|

Did you know you that a business can have a positive net income, but still be bleed money? In Part I we talked about the Balance Sheet (your net worth) and in Part II we talked about the Income Statement. The problem with the Income Statement is that it only shows your expenses... and things like paying down the principal portion of your loans are not expenses. If you rely solely on your Income Statement to do your budget, you could be in for a rude surprise if you carry a mortgage. This is where the Statement of Cash Flows comes in. The point of the Income Statement is to help explain changes in your net worth. This is not the same thing as the change in your cash balance. The Statement of Cash Flows In the corporate world, a company's Statement of Cash Flows is organized into the following three parts:

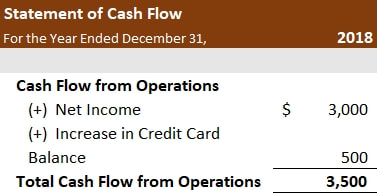

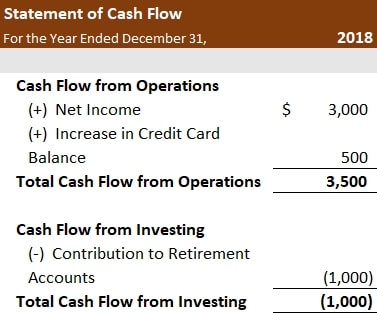

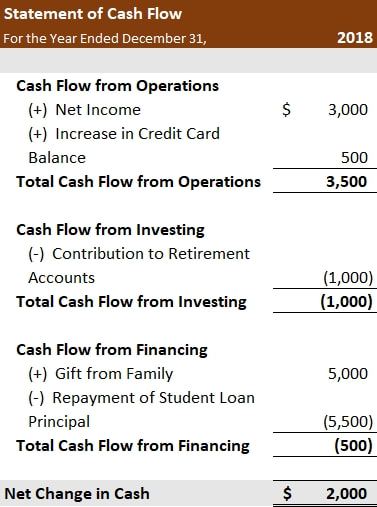

This article will talk about how you can apply each of these to your own finances to help you budget or see if you are running out of cash. Cash flow from Operations The purpose of this part of the statement will be to show how much money you are bringing in from your job(s) and how much is left over after you account for the expenses you incur while living your life. This section starts out as your Net Income from the Income Statement. 1. Put down the number you came up with for Net Income in your Income Statement. That number is your starting point. The next step will be to make a few adjustments to that number. The point of the Cash Flow Statement is to show how you got from whatever you had in your bank account the year before to what you have as of the date of the report. This means you need to back out everything you paid using your credit card that you didn't pay off. Here is how you do it... 2. (a) Add back money for the expenses you didn't pay cash for. If you bought $1,000 worth of stuff on a credit card and haven't paid it off yet, you need to add this money back as an adjustment. You are supposed to be showing Cash Flow, and in such an example, the cash hasn't really "flowed" yet. When you finally pay this stuff off next year, you will be subtracting it back (see Step 3) in next year's statement (not this year's). Another example... on your Income Statement, you are supposed to list how much taxes you were supposed to pay as an expense (as opposed to only what was withheld). When you do your taxes and it says you were supposed to pay $10,000, that's what you put on your Income Statement as an expense. If they only withheld $9,500, this is where you add back the $500 you didn't pay yet. 2. (b) Add money for the cash you got back for things owed to you from prior years (like the tax refund check you got during the year of your Statement). On the other hand let's say you got a tax refund check in 2018 for $800 for 2017's taxes. On 2018's statement, you need to add this $800 to your Cash Flow from Operations. 3. (a) Subtract payments that you made for past year's expenses.* This is the opposite of Step 2 (a). Let's say you bought $1,000 worth of stuff using a credit card in 2017, but didn't pay it off. You still owe that $1,000 in 2018. If you finally decide to pay it off in 2018, you need to subtract that money from your Net Income. The cash finally "flowed" this year. In Step 2(a), I mentioned the example of $500 you have to pay to the IRS in taxes in 2018 because they withheld too little in 2017. You need to subtract this from your 2018 statement. *Remember, in the Cash Flows from Operations piece, do this only for expenses. This is not for principal payments used to acquire assets that went on your Balance Sheet. Buying an asset is an Investment, not an Expense. Also, do not do this for payments on expenses that you already counted in this year's Income Statement. 3. (b) Subtract money for the cash you were supposed to get based on the Income Statement but didn't (like the refund you will be getting the year after the one on the Statement) This is the opposite of Step 2 (b). If you are doing a statement for 2018 and you are getting a tax refund in 2019, you need to subtract the amount of the refund from 2018's statement. The tax expense that's part of Net Income is supposed to be based on the actual taxes you owe (which you calculate when you do your taxes the following spring) not what's been withheld. Your Net Income is saying that your actual tax expense is lower than what actually got withheld. This is why you subtract it out, because that difference in cash isn't in your bank account yet. Let's do a simple example for the Cash Flow from Operations. If you recall from the Income Statement article, Brian had a Net Income of $3,000. The balance on his credit card increased by $500 from last year because he used his credit card for some of his expenses but didn't pay it off.  Per Step 2(a), Brian has to add this $500 back because he didn't pay it off yet. Cash flow from Investing 4. Add up the distributions you took from investment and retirement accounts. Then subtract the contributions you made. The total (either positive or negative) is your Cash Flow from Investing. The money that you transferred from your investment accounts / IRA / 401k plan, real estate portfolio into your bank account as cash ... write this number down. This is a Cash Flow from Investing. It's flowing to your bank account so it should be added. The money you contributed to those accounts or real estate you bought? Write this number down and subtract it from the number above. This is a Cash Flow to Investing. It's flowing away from your bank account so it should be subtracted. If you are in the accumulation phase of your life (ie, you are not retired) the net number for Cash Flow from Investing will probably be negative, while your Cash Flow from Operations will be positive. When you retire and start drawing down on investments, it will be the other way around. In the Brian example, he contributed $1,000 to a retirement account in 2018. This is how it looks on the Cash Flow from Investing.  Cash Flow from Financing 5. Add up the money you received from loans you took out to purchase assets (such as a house). Also add gifts of money you got. Then subtract the principal payments on the loans you took out to purchase assets. The total (either positive or negative) is your Cash Flow from Financing. If the bank gave you a $200,000 mortgage to buy a house, that $200,000 is a cash flow from Financing. If your rich uncle Louie gave you a gift of $5,000 for your wedding, that would also go here. As far as outflows go, remember back in the Income Statement how we only counted interest expense on the Income Statement and left off principal? This section is where that goes. In 2018, Brian paid $6,000 on his student loans, of which $5,500 was principal. The interest piece was already included as part of Net Income, so only the $5,500 gets shown as a subtraction. Also, his parents had given him $5,000 to help him out with his loan situation. That is shown as an addition.  If you are not sure whether to add or subtract something, think of it like this... If something otherwise makes your Cash balance higher (for example - [1] not making a payment, or [2] receiving a gift of money), add. If it makes your Cash balance lower (for example - [1] making a payment, or [2] not receiving cash you were supposed to get), subtract. After all, notice how the last line says Net Change in Cash? 6. Add together the totals from [1] the Cash Flow from Operations, [2] the Cash Flow from Investing, and [3] the Cash Flow from Financing. The total is your Net Change in Cash. The total you get for the Net Change in Cash should be equal to [1] the amount you showed as Cash on your Balance Sheet this year minus [2] what you showed as Cash the year before. If it doesn't, then you made a mistake somewhere. How nit picky you want to be about this is up to you (as long as you're not off by much). Personally, I make sure I tie out to the penny. There's an important takeaway from all three of the statements in this series of articles (Balance Sheet, Income Statement, and Statement of Cash Flows). Someone who is financially healthy will have the following profile:

In the final part of this series, I will show a more complicated example showing a fictional, but realistic household's finances.

0 Comments

Leave a Reply. |

Broken Ticker

An alternative minded Investing and Personal Finance blog Archives

February 2019

Categories

All

|

RSS Feed

RSS Feed