|

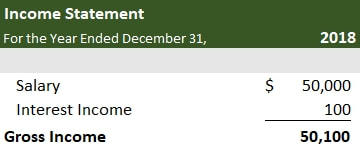

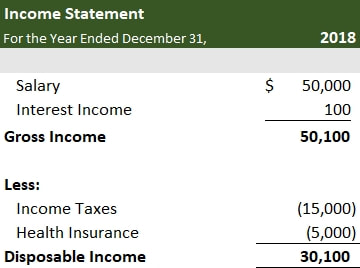

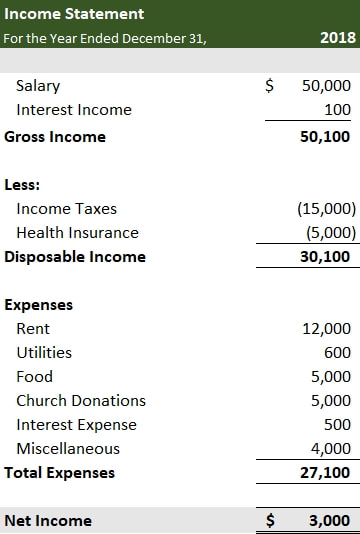

Your household isn't really much different from a business. You generate revenue (you and your spouse's salaries, for example) and like a business, you also have expenses (rent payments, grocery bills, etc). Any good business owner or CEO knows whether his company is making or losing money. If someone asked you if you made or lost money last year, would you know? In Part I of the Making your own financial statements series, I talked about how to calculate your net worth by replicating the first of the three reports that make up a publicly traded corporation's Financial Statements. In this part we will discuss the second report, which is called the Income Statement. The Income Statement The income statement is where you find out whether you're making or losing money. In this article I will discuss how you can make one and organize it in a format that's relevant for you. Gross Income The first part is your gross income. This is your top line of revenues before any taxes, deductions, or expenses. 1. List all your sources of income along with the amounts before any taxes, deductions, or expenses. What was the year to date gross salary/wage from your last pay stub of the year? How much did you earn in interest on your savings accounts? etc... Write these down and come up with a total. You should include the realized gains or losses from any stocks or investments you own here too. Realized means you sold them during the year. Losses obviously get subtracted from your gross income. Do not include the gains/losses from retirement accounts that you can't access yet. The fact that they go up or down in value doesn't really say anything about how you make a living. Therefore they don't belong on your income statement. Let's go back to Brian from Part I. Brian is salaried and made $50,000 a year on his job (gross, or before taxes and deductions) in 2018. His December bank statement said he made $100 in interest on the year. Here is the first part of his income statement:  Disposable Income The next step is to list your paycheck deductions and get down to your disposable income. This step is useful because unlike the gross income above it, this is how much money you have available for spending or saving. 2. List your deductions along with the amount.* How much taxes were deducted? How much did your employer deduct for health insurance? etc... Write these down and subtract them from your gross income. Sometimes your employer deducts too much or too little in taxes and you end up getting a refund or having to mail a check to the government. I will show you how to deal with these situations in Part IV when I do the complex example. For now let's assume that the amount deducted is equal to the amount you actually owe. *This part is important... do not list paycheck deductions to a defined contribution plan like a 401K. I will explain why when we get to expenses. The only deductions you subtract are for money you will never see again like taxes, health insurance premiums, or deductions for a defined benefit pension plan. Brian had $15,000 in income taxes deducted from his paycheck. His employer also deducted $5,000 for his health insurance.  Expenses The final step is to itemize your expenses. Expenses reduce the value of your assets without also reducing your debt. Remember the Assets = Debt + Equity equation from Part I? If Assets go down, and Debt is unchanged, Equity (your net worth) has to go down in order for the equation to balance. In other words, expenses reduce Equity. For example, if you spend money on something, money comes out of your bank account and your Total Assets from the Balance Sheet get reduced. Your net worth goes down by that same amount. The only exception is if you buy another asset of value that you can put back on your balance sheet (like a house). In such a case, even though Cash still gets reduced, your house gets added back on... the overall total is not reduced because the two things offset each other. The Total Assets line, and thus your net worth, remain the same. Same thing with retirement account contributions (for defined contribution plans). They come out of your paycheck, but get added back on your balance sheet under Retirement Accounts. This is why they are not expenses. Rearranging things under Assets is not an expense, it's an investment. Here's a tricky example... the principal on your loan payments... these are not expenses either. Why not? The payment reduces your cash, but also your debt, leaving equity unchanged. Remember, if equity is unchanged, it is not an expense. Only the interest portion is an expense. Bottom line... it's an expense only if you are forced to decrease equity to balance out the equation. 3. Itemize your expenses along with the amounts. How much did you pay for rent? How much did you spend on food? etc... Write these down and come up with a total. Be as specific or as general as you want to be here. It's your annual report. More details will mean more work, but you'll also learn more about where you're going financially. 4. Subtract your total expenses from your disposable income in Step 2. This is your net income. In 2015, Brian's rent was $1,000 a month ($12,000 a year). He spent $600 a year on utilities and $5,000 on food. He gave another $5,000 to his church. He made $6,000 in payments on his student loans, of which $500 was interest and $5,500 was principal. His other expenses totaled $4,000.  As you can see, Brian's net income for the year is $3,000 which means he is making money and adding to his net worth (equity). In the next part (the Statement of Cash Flows), we will talk about a big limitation with the Income Statement and what to do about it. You may have noticed it already. "Wait a second! I paid $6,000 in loans. Why am I only putting down $500? The remaining $5,500 is still money out the door! My bank account didn't go up by $3,000. My bank account went down! How are you telling me that I made $3,000?" If that is your reaction then you are missing the point. The point of the Income Statement is to explain the change in your Net Worth, not how much cash you are bringing in (or bleeding). That is why you also need a Cash Flow statement (Part III).

0 Comments

Leave a Reply. |

Broken Ticker

An alternative minded Investing and Personal Finance blog Archives

February 2019

Categories

All

|

RSS Feed

RSS Feed