|

Buy and Hold is a passive investment strategy that involves buying stocks and holding them for long periods of time... never selling regardless of what's happening in the market. Although it can be used with individual stocks, this article will discuss the merits (or not) of this strategy as applied to index funds tracking the S&P 500, which are a popular and low cost way for the average investor to "be in the market". This strategy is often combined with a technique called Dollar Cost Averaging, where you contribute to your investment account and buy the stock/fund at whatever price it's trading at at the time of the contribution. Also known as a "set it and forget it" strategy, it's touted by many as the best way to invest for the average Joe.  Anyone else remember the Ronco Grill? Proponents of buy and hold claim that when individuals try to time the market instead, psychological factors get the best of them... when the market is crashing, they panic and sell at a loss... when the market turns around, they hesitate and miss out on gains... when the market really starts taking off, they finally get in at higher prices than when they sold... Instead of "buying low and selling high", which is what they try to do, they end up "buying high and selling low"... leading to worse returns than if they had just bought and held. These accusations are not without merit. According to various business articles on the internet, the average investor consistently under-performs the S&P 500 by a few percentage points. In fact, according to Business Insider, a study by Fidelity showed that the best performing investors... were dead... in second place were those who had forgotten they had an account. Now, none of these articles pointed to freely available hard data or legitimate sources, so you decide for yourself whether they're true or horse hockey. They probably are pure sensationalism and yellow journalism (especially the supposed Fidelity study), but if you think about the people you know, or even yourself, this idea of the average investor under-performing is not too crazy. Proponents of buy and hold say that instead of timing the market, investors should focus on time in the market, referring to the tendency of the market to rise over the long term. However there are a couple of things they are not telling you. Buy and hold only works when the following two conditions are met:

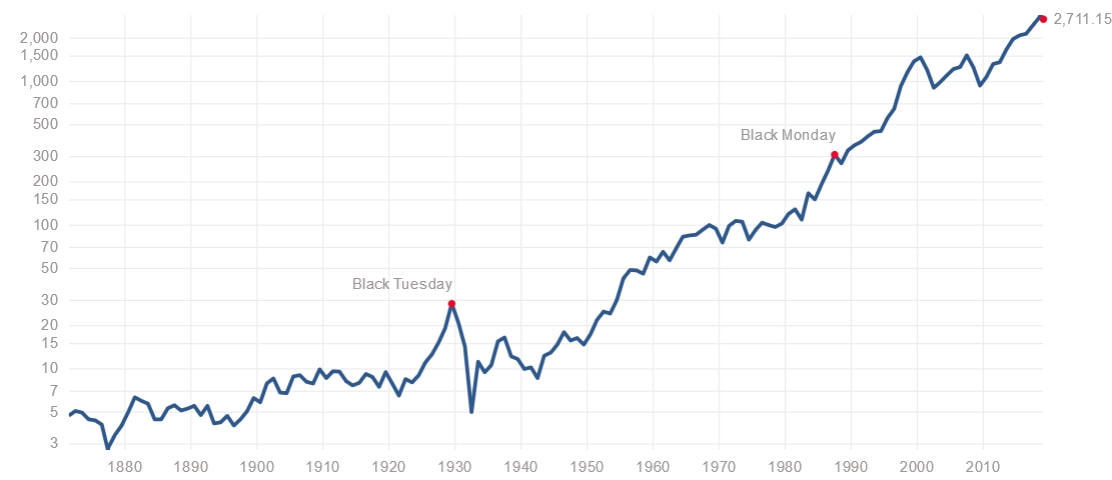

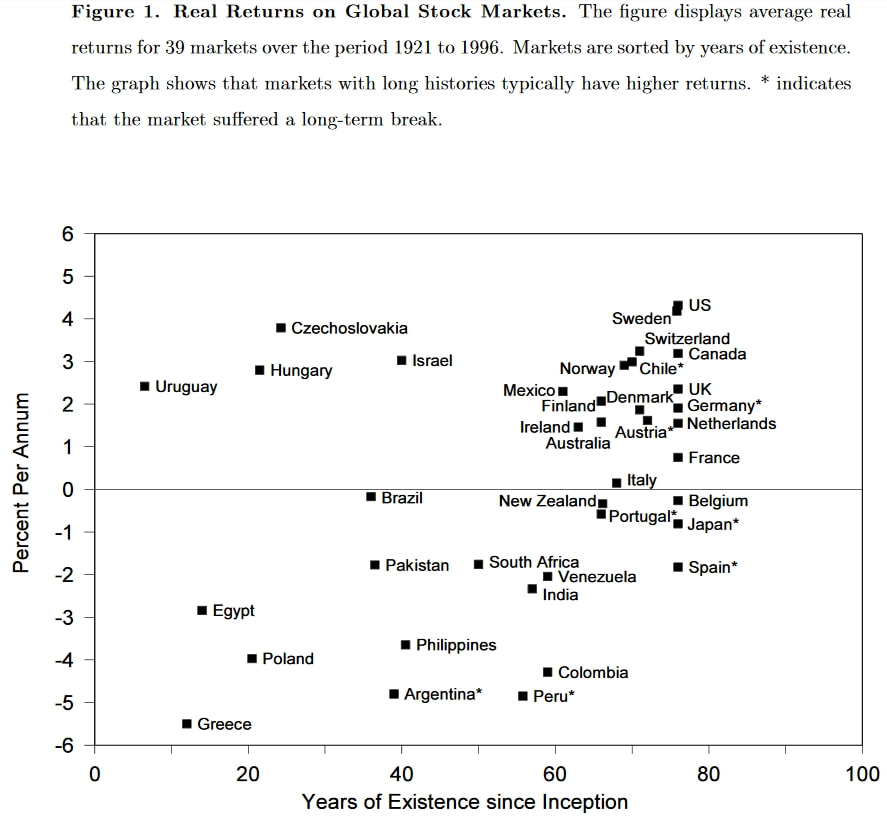

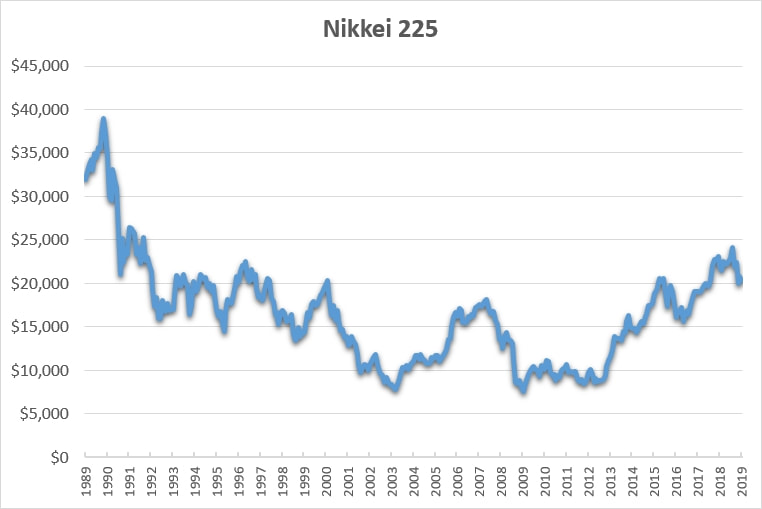

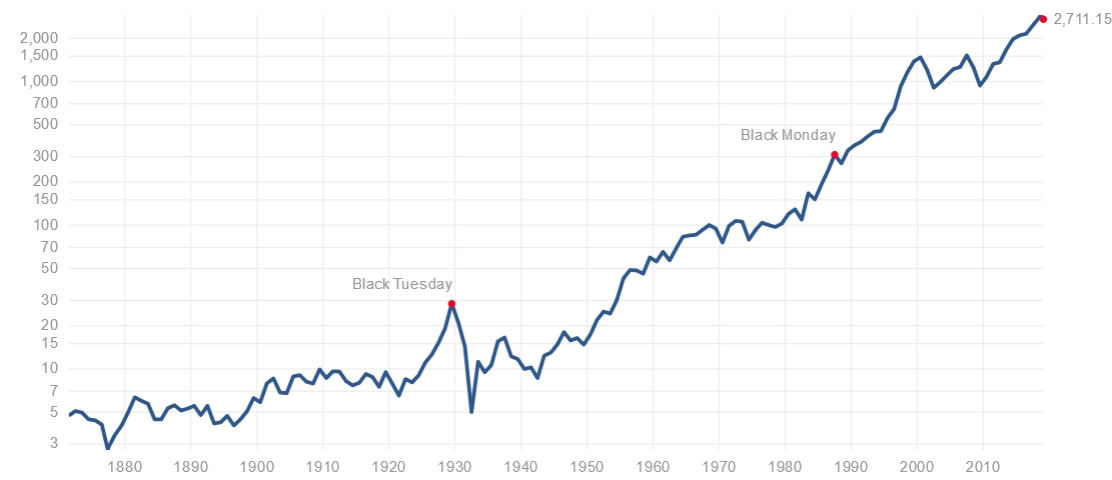

Let us focus on these two conditions separately and then you can decide for yourself if buy and hold is for you. Condition #1: A long term positive trend exists Those of us living and investing in the United States have been fortunate enough to have enjoyed a period of over 200 years of positive double digit nominal returns on equities.  Source: http://www.multpl.com/s-p-500-historical-prices We have been conditioned and accustomed to believe that this is normal and how things should be. Is it? Here is a chart from an academic paper showing global equity market returns in the 20th century. Notice how the US is a bit of an outlier in the top right.  Source: Global Stock Markets in the 20th Century. Jorion & Goetzmann Those from the Buy and Hold camp who are critics of both (a) market timing, and (b) the use of technical indicators to do so often say that such methods "work... until they don't". Not that I'm advocating for such methods in this article, but these folks are guilty of the same thing. By "setting and forgetting", you are banking on the current positive trend in US equities continuing. You are also exposing yourself to the "black swan" risk of it not. Here is a story about a turkey from the book The Black Swan by Nassim Taleb... the turkey is fed and cared for by the farmer day after day. The turkey thinks this is normal and that the farmer is his friend. "On the afternoon of the Wednesday before Thanksgiving, something unexpected will happen to the turkey. It will incur a revision of belief." It may not happen all at once like with the turkey, but... Ask yourself this... Is the Roman Empire still around? How about the once mighty British colonial empire? Everyone's turn at the top eventually comes to an end and the United States will be no exception. Will it happen in our lifetimes? Maybe not... but continuing double digit returns into perpetuity should not be a foregone conclusion. If returns ever flatten out over the long term, or decline, Buy and Hold will stop working. Take a look at the returns of the Japanese stock market over the last 30 years.  Japan was a worldwide economic powerhouse through the 1980's and at one point people were predicting that it was going to overtake the United States. What happened since? Almost 30+ years of market returns going nowhere. This is not likely to change anytime soon given the demographic challenges of their aging population. How did Buy and Hold work there? How about Russian investors in 1917? Like market timing, Buy and Hold works... until it doesn't. But let's assume that the long term trend remains intact during our lifetimes. The second condition for Buy and Hold to work is that: Condition #2: Your investment horizon is long enough The interesting thing about that first chart of the S&P 500 is that if you had invested a few thousand dollars in 1880 and sat on it, you would be a multi-millionaire today. You would also be over 139 years old. Here is the chart again:  Source: http://www.multpl.com/s-p-500-historical-prices No one has 100+ years to ride out the market cycles and volatility. A more realistic time horizon is 30 or 40 years. Take a closer look at the chart though and you will notice a few 20 year periods here and there where stocks went nowhere. And as you accumulate money over your working life, the returns at the end count more than at the beginning. It's called sequence of return risk. A 40% market drop when you are only 20 years old with just $5,000 in your account hurts a lot less than the same thing happening to a 65 year old with $1 million ready to retire. If you Dollar Cost Average along with set it and forget it, you need to worry about birthday risk. It's the risk that the year of your retirement comes right as the market drops and enters one of those 20 year periods of going nowhere. It's called birthday risk because you were born (and thus will retire) in the wrong decade to make money. This is why even if you Buy and Hold, a good idea would be to at least manage your asset allocations and reduce risk as you get closer to retirement, as opposed to just "setting it and forgetting it".

0 Comments

Leave a Reply. |

Broken Ticker

An alternative minded Investing and Personal Finance blog Archives

February 2019

Categories

All

|

RSS Feed

RSS Feed